At the same time, the market is not expressing great confidence in the Republicans ability to control 51 seats (remember that under this contract, only a Joe Miller victory would accrue to the Republicans in determining control).

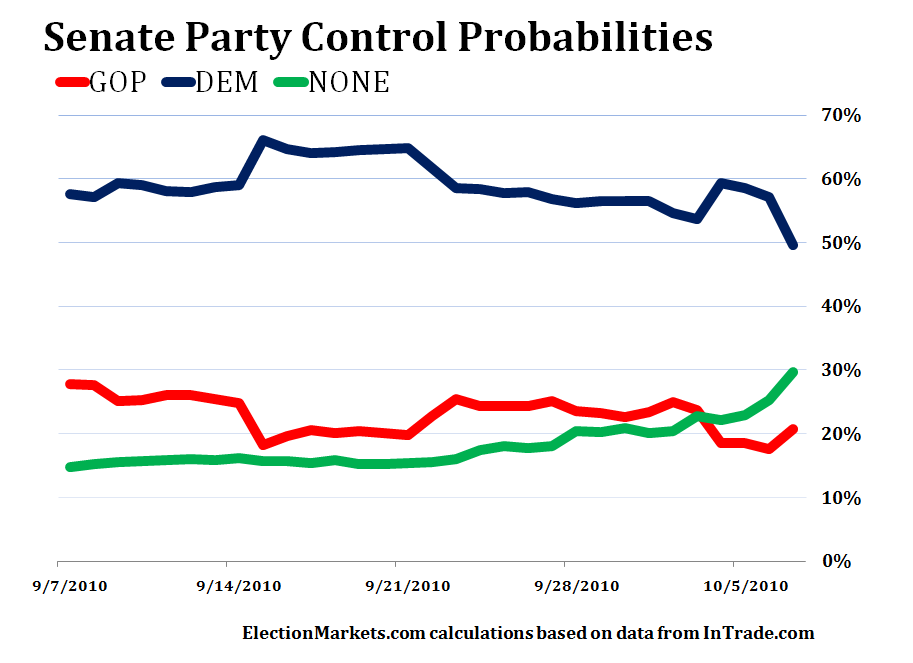

The trend in the Senate has clearly favored Republicans over the past month. The question is whether of not that trend will accelerate over the next three weeks, sputter, or reverse.

On the House side of the ledger, the Republican probability of control stands above 74%. Republicans are clearly in the driver's seat according to market pricing. The midpoint estimate of 226 seats would be an improvement of 49 seats from the 177 seats Republicans held after the 2008 elections.

Observers should recognize that at this point in the cycle we are likely to see the seat projection begin to show greater variance than the control probabilities where the House elections are concerned.

Back to the Senate side ... As the following chart to the left illustrates, the shift in the expected distribution over the past month has been to the right (favoring Republicans) even with markets' discounting of Republican chances based on the Murkowski announcement of a write-in campaign and the negative perception of Christine O'Donnell's chances in Delaware.

{kind=link}

As noted yesterday, the pricing presently suggests that control of the Senate may likely come down to three Senate races -- Illinois, Nevada, and Washington -- but could quickly expand to include additional states like California.

The following table -- outlines the current probability estimates in the 37 Senate races.